Buying a home is, for the vast majority of Hong Kong people, the largest leveraged investment of their lifetime. While second-hand properties offer higher efficiency rates and mature neighborhoods, they are like thick history books. Every crack and every trace of peeling paint records the living habits of previous tenants and the maintenance standards of the building. If you buy a property based solely on “feeling,” this 30-year mortgage marathon could easily turn into a nightmare.

For first-time homebuyers in Hong Kong, the purchasing process can be confusing, making access to sufficient information absolutely crucial. The second-hand property market is not just a comparison of prices; it involves numerous hidden financial risks and legal liabilities. Making the right real estate investment decision lays the foundation for future financial freedom. Therefore, a deep understanding of a property’s value and its potential issues will help you avoid future troubles.

This guide is designed not only to help you find the right property but also to elevate your professional knowledge, enabling you to make informed choices during the buying process. Through deep market research, you can gain a clearer understanding of the challenges and opportunities you face.

This comprehensive guide will clear all your blind spots across four dimensions: Physical Inspection, Legal Verification, Financial Actuary, and Psychological Warfare.

This article provides relevant data, case studies, and expert opinions to help you comprehensively understand how the second-hand property market operates. Additionally, we will share the experiences of successful homebuyers so you can draw inspiration and learn from their lessons.

Before diving into specific inspections and preparations, it is recommended that you develop a detailed plan listing all factors to consider. This ensures no critical details are overlooked at any step.

The land search process is more than just verifying the owner’s identity; it requires a deep dive into the property’s historical background. By reviewing legal documents and historical records, you can uncover many underlying issues—such as whether previous tenants had unresolved disputes or debts.

Chapter 1: Intelligence First — The “Information War” Before Property Inspection

For example, if a land search reveals that the property was involved in lawsuits in the past, this could heavily impact your buying decision. This type of information is sometimes concealed by owners, so you must remain vigilant and ensure all data is transparent and credible.

Furthermore, any outstanding legal issues will jeopardize your purchasing rights. Therefore, before entering into any transaction, be sure to carefully scrutinize all legal documents and seek professional legal advice if necessary.

Many novices start their property search by looking at the posters outside real estate agencies—this is a mistake. The real property inspection begins in front of your computer screen.

Taking it a step further, when dealing with bank valuations, understanding the criteria and processes of multiple banks becomes exceptionally important. Different banks have varying appraisal standards. It is advised to communicate with multiple banks in advance to obtain their valuation reports, allowing you to make a thorough comparison and select the most suitable financial institution for your mortgage.

1. Decoding Hidden Messages in the “Land Search”

A Land Search (Land Registry record) is the property’s “medical history.” Beyond checking who the owner is, you must look closely at the “Remarks” column:

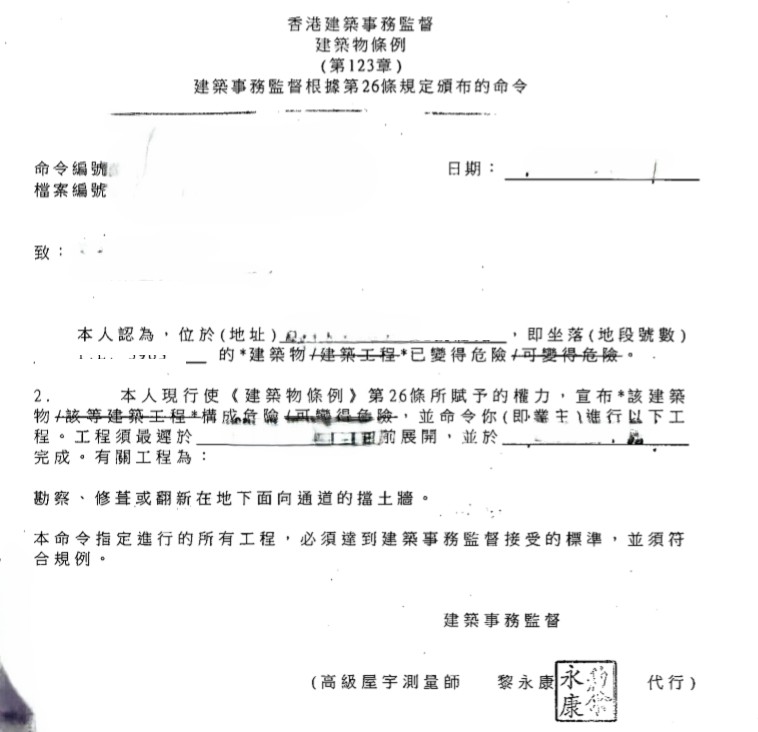

- Building Order (issued by the Buildings Department): This usually involves illegal structures. If the unit has an unapproved enclosed balcony or a demolished structural wall, banks are highly likely to reject the mortgage outright.

- Lis Pendens (Pending Lawsuit): This indicates the property is entangled in a lawsuit. It could mean the owner is being sued for debt, or there is an inheritance dispute. The legal rights of such properties remain extremely blurry until the lawsuit is settled.

- Charging Order: Commonly known as “nailing the deed” (釘契). This is most frequently caused by unpaid management fees or major building maintenance costs. Although the seller is obligated to clear this before closing, it reflects that the owner’s financial situation may be extremely strained.

2. The “Three Kingdoms War” of Bank Valuations

During the physical inspection process, apart from checking the condition inside the unit, you should also consider the impact of the surrounding environment. For instance, nearby transport convenience, commercial facilities, and school resources will directly affect the comfort and convenience of your future living environment.

Additionally, relationships with neighbors are a factor that cannot be ignored. Understanding your neighbors’ living habits and their impact on the community can help you better judge whether the property’s living environment suits you.

Never blindly trust an agent who says a property “can meet the valuation.” Before signing the Provisional Agreement for Sale and Purchase (PASP), you must personally call or use online tools to consult at least three banks.

- Valuation Gap: If the transaction price is HK$8 million but the bank only values it at HK$7.5 million, the mortgage loan-to-value ratio will be calculated based on HK$7.5 million. You must make up this HK$500,000 difference in cash. This is the most common hidden cause of mortgage defaults.

Chapter 2: On-Site Inspection — A Checklist of 15 Hidden Pitfalls

When you walk into a unit, do not be misled by the faint aroma of scented candles or soft background music. What you need are the eyes of a professional building inspector.

1. “Secret Signals” of Water Seepage: Skirting Boards and Ceilings

Of course, legal details in real estate transactions are also crucial; it is not just a matter of signing a contract. Understanding potential traps in a contract will help you avoid legal disputes in the future.

Water seepage is the cancer of second-hand properties. Check the wooden skirting boards at the base of the walls. If they are blackened, deformed, or show peeling paint, there is a high probability of under-floor pipe leaks or waterproofing failure in the adjacent bathroom. When checking ceilings, focus on the area below air conditioners and the ceilings of kitchens and bathrooms. Water stains or mold spots here can easily cost tens of thousands of dollars to repair.

2. Integrity of Structural Walls (Main Walls)

Since the “LOHAS Park Incident,” altering structural walls has become a legal red line. Compare the unit with the original developer’s floor plan. If you find a wall between two rooms has been removed, you must confirm it was a non-structural wall. If a structural wall is suspected to have been demolished, the bank will demand a reinstatement certificate; otherwise, they will refuse the loan.

3. The Safety “Fatal Point” of Aluminum Windows

Check the rivets on the window frames. If they show a white, powdery residue, it means they are severely oxidized, posing a risk of falling into the street during typhoons. Also, open the windows to see if the latches are loose. Replacing all aluminum windows in a flat adds at least HK$50,000 to HK$100,000 to your budget.

4. The “Chain Reaction” of Water Pressure and Drainage

Turn on all faucets in the flat simultaneously and flush the toilet. If the water pressure drops significantly, the building’s communal pipes may be rusted or clogged. This is a systemic risk for the entire building, not something you can fix with your own interior renovation.

5. Illegal Structures: Balconies and Kitchens

Many older buildings have balconies enclosed to create a room, or kitchens converted into open-plan layouts. If the original floor plan does not show an open kitchen, and it lacks an automatic sprinkler system and a fire-rated door, it constitutes an illegal alteration. This will invalidate insurance and stall mortgage approvals.

6. The “Time Bomb” of Hollow Tiles

Use a tile inspection rod to gently tap the wall tiles in the bathroom and kitchen. A hollow sound indicates uneven cement plastering. In such cases, tiles can fall off and cause injuries at any time, or allow moisture to seep into the walls, causing large-scale mold.

7. Aging of the Electrical System

Open the distribution box (fuse box) to see if it uses old-fashioned fuses or modern Miniature Circuit Breakers (MCB). An old fuse box usually means the wiring throughout the flat has been used for over 30 years and must be completely rewired—an expense that starts at HK$100,000.

8. Air Conditioning Costs in “West-Facing” Flats

Hong Kong summers are long and scorching. Inspecting a property between 4:00 PM and 6:00 PM yields the most accurate results. The walls of west-facing flats absorb heat and remain hot to the touch even at 2:00 AM. Over time, this not only damages furniture but also increases monthly air conditioning bills by 40% compared to normal units.

9. Neighbors’ “Quality Signals”

Observe the corridor. Is it cluttered with trash and belongings? Are there unusual odors? More importantly, look at whether neighbors have installed multiple CCTV cameras outside their doors. This often hints at severe neighbor disputes or security issues on that floor.

10. The “Shelf Life” of the View

Does the open park view you see now happen to be marked for residential use on the Statutory Outline Zoning Plan (OZP)? If so, in two years, you will be facing construction noise and dust, along with a price drop once the view completely disappears.

11. The “Money Pit” of Building Maintenance

The biggest fear when buying a second-hand property is major building maintenance. Ask the management office: Has the building recently received a “Mandatory Building Inspection Notice”? How much is left in the maintenance fund? If the fund is insufficient and work is about to begin, you may have to pay a HK$100,000 to HK$300,000 “maintenance contribution” right after moving in.

12. Ventilation and Health in “Windowless Bathrooms” (Black Toilets)

“Black toilets” (bathrooms without windows) rely heavily on mechanical ventilation. Check the power of the exhaust fan and look out for back-flowing odors. If poorly managed, windowless bathrooms easily breed mold, presenting a health threat to family members with allergies.

13. The “Scaffolding Cost” of Air Conditioner Placement

Observe where the air conditioners are located. If poorly designed, every maintenance job (or even just a routine cleaning) will require outdoor scaffolding, with fees starting from HK$5,000. This is a long-term holding cost of the property that should not be ignored.

14. Proximity to the Refuse Room

Units near the refuse room may offer convenience for throwing away trash, but the resulting cockroaches and odor issues can drive you crazy. Especially in summer, if the refuse room’s negative pressure system fails, smells will travel down the corridor and straight into your home.

15. Cross-Checking “Stigmatized Properties” (Haunted Houses)

In addition to asking your agent, you must personally input the property address into the online valuation systems of various banks. If a bank displays “Call valuation” or shows an abnormally low valuation, the property is highly likely a “haunted house” or has a history of severe unfortunate events.

Chapter 3: Legal Traps — Don’t Sign Away Your Tears on a Contract

After inspecting the property, placing a deposit and signing documents is another battlefield.

1. The 5-Year Forbidden Zone of a “Deed of Gift”

This is the most fatal trap. If the seller acquired the property via a gift (or an exceptionally low-priced transfer), under the Bankruptcy Ordinance, creditors have the right to reclaim the property if the original owner goes bankrupt within five years. No bank will approve a mortgage for a property tied to a Deed of Gift that is less than five years old. If you accidentally sign the contract, you must “Full Pay” in cash, or forfeit your deposit.

2. Misinterpreting “As-is Basis”

Many buyers tend to overlook the additional expenses incurred during the home purchase process, and these miscellaneous fees can significantly inflate the total expenditure. Understanding all possible costs and planning ahead is vital to ensuring a stable cash flow.

When performing financial calculations, you should consider all conditions that could affect mortgages and loans—including interest rate fluctuations and market volatility—as these factors can impact your repayment ability.

Contracts often state that the property is sold on an “as-is basis.” Owners will use this as an excuse to refuse fixing leaks discovered after you sign the agreement.

The Fix: Insert a clause into the provisional agreement requiring the seller to guarantee that the structural walls, plumbing/electrical systems, and home appliances are in normal working condition prior to hand-over.

3. The “Marathon” Procedure of Probate Deeds

When buying a property under a probate deed (inherited property), you must ensure that all beneficiaries agree to the sale. If even one beneficiary objects or goes missing, the transaction can be delayed indefinitely, locking your funds up in the law firm’s escrow account.

Chapter 4: Financial Actuary — How Much Cash Do You Need Besides the Down Payment?

Many people assume that preparing a 10% down payment is enough. In the second-hand market, this assumption is extremely dangerous.

During negotiations, remember to leverage the information you have gathered to support your requests. This can effectively increase the likelihood of successful bargaining. Providing concrete examples will make your demands far more persuasive.

1. Checklist of Taxes and Miscellaneous Fees

You must reserve roughly 5% to 8% of the property price for miscellaneous expenses:

- Stamp Duty: For first-time HKPR buyers, properties up to HK$4M pay only HK$100; above HK$4M, rates scale up from 1.5% to 4.25%. For a typical HK$8M flat, expect roughly HK$240,000 in stamp duty.” Note also that there was a 2026-27 Budget change increasing the AVD rate for residential properties above HK$100M from 4.25% to 6.5% (effective 26 Feb 2026)

- Agency Commission: Typically 1% of the property price.

- Legal Fees: For handling title deeds and mortgage contracts.

- Mortgage Insurance Programme (MIP): If you take out a 90% mortgage, this premium can cost 2% to 5% of the loan amount. Though it can be financed into the mortgage, it increases your monthly payments.

2. The Risk of a “Shrinking” Mortgage Tenor

Banks usually calculate the maximum mortgage loan tenor using “75 minus building age” or “80 minus building age.”

Case Study: If you buy an older property with a building age of 50 years, the bank may only approve a 25-year or even shorter mortgage tenor. This means your monthly repayments will be significantly higher than expected, directly challenging your income requirements.

Throughout the entire process, continuously maintain your rationality and calm. This ensures your final purchasing decision is based on actual data and thorough market research, rather than pure emotional factors.

Chapter 5: Advanced Negotiation Tactics — Using Defects to “Buy Down” the Price

The flaws you discover during property inspections are your most powerful bargaining chips.

- “Data-Driven” Price Reduction: Do not just say “the renovation is old.” Instead, say: “The air conditioning drainage pipes are leaking, and redoing the waterproofing for the whole flat will cost HK$150,000. I would like to deduct this repair cost from the property price.”

- Major Maintenance Psychological Warfare: If the building is about to undergo major repairs, you can capitalize on the owner’s mindset of “wanting to avoid hassle and cash out” by demanding that they reserve a sum for the building maintenance fund.

- The Valuation vs. Budget Gap: Confront the owner directly with the bank’s valuation sheet: “I want to buy, but the bank cannot meet your asking price. Unless you lower the price, I won’t be able to secure the loan.”

Ultimately, buying a home is not just a transaction process; it is a choice about your future quality of life. Remember, this second-hand property inspection guide should be an essential tool in your arsenal, helping you make the wisest choices in a complex market.

Rationality is the Insurance for Your Brain

Buying a second-hand property is a tug-of-war with the owner, the building, and time. In this process, “not buying” is always a valid option.

In summary, this property inspection guide serves as a comprehensive roadmap, providing vital information and advice for every prospective buyer to help you find your ideal home in the second-hand market.

When you are drawn to beautiful furniture, force yourself to look at the blackened corners of the walls. When an agent urges you to place a deposit, force yourself to call the banks for a valuation. An excellent buyer does not daydream in a beautiful living room; they calculate repair budgets under a damp bathroom ceiling.

Hopefully, this guide will serve as your compass in the property market, helping you steer clear of all hidden traps and secure a truly desirable, stable home.

【Property Inspection Checklist (Final Check)】

- [ ] Land Search: Any Order 24/26? Any inheritance/probate disputes?

- [ ] Water Seepage: Any water stains on the ceiling? Any blackening on the skirting boards?

- [ ] Structure: Have any structural walls been removed? Is there a fire safety certificate for the open kitchen?

- [ ] Valuation: Can three banks fully match the transaction price in their valuations?

- [ ] Maintenance: What is the balance of the building’s maintenance fund? Are there maintenance plans for the next five years?

- [ ] Neighborhood: The corridor environment, whether neighbors have installed CCTVs, any noise issues.

- [ ] Legal: Is it a Deed of Gift? Is it a Probate Deed? Is the completion period long enough for the bank to approve the mortgage?

Wishing you a smooth journey through this major milestone in life. Happy home hunting!